ACAG Scheme Loan Eligibility

ACAG Scheme Loan Eligibility For many families in Punjab, owning a small residential plot is a blessing that still feels incomplete. The dream of building a house often remains unfulfilled due to rising construction costs, low income, and lack of access to bank financing. Over the years, I have seen countless families living in rented portions while their own plots remain empty because construction is simply unaffordable.

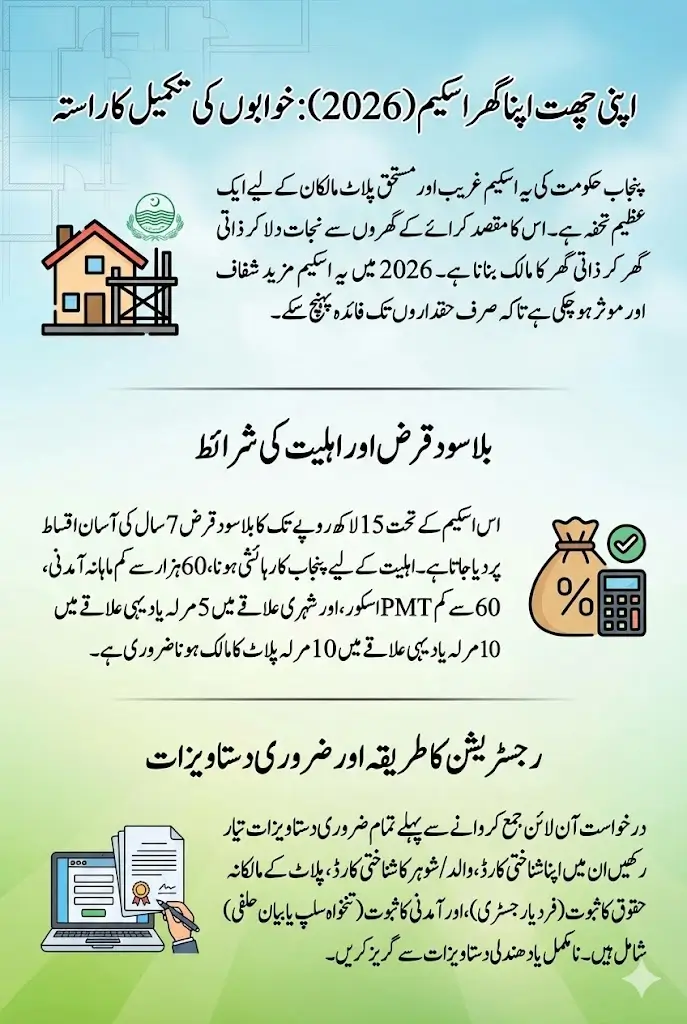

To address this long-standing problem, the Punjab Government introduced the Apni Chhat Apna Ghar (ACAG) Construction Loan, an interest-free loan designed only for deserving plot owners. As we move into 2026, this scheme has gained more attention due to its transparent online system, strict eligibility checks, and clear focus on low-income households. This guide explains everything in simple words so even an ordinary citizen can understand how to qualify and apply.

You Can Also Read: Apni Chhat Apna Ghar Program

What Is the ACAG Construction Loan and Why It Matters in 2026

The ACAG Construction Loan is not a commercial loan and it is not meant for profit. It is a government-backed, zero-interest housing loan that helps families construct a basic residential house on land they already own. Unlike private banks, the government does not charge interest, making it possible for poor families to repay the loan without financial pressure.

In 2026, this scheme has become even more important because construction material prices, labour costs, and rent have all increased sharply. Many families are paying high monthly rent while their own plots lie unused. Through ACAG, the government is trying to convert these empty plots into livable homes, improving living conditions and reducing housing insecurity across Punjab.

Why this scheme matters today:

- Construction costs are beyond the reach of low-income families

- Banks usually reject poor applicants or charge heavy interest

- The scheme promotes self-owned housing instead of rental dependence

- Online tracking reduces corruption and middlemen involvement

Who Can Apply for the ACAG Loan in Punjab

The ACAG scheme is designed only for deserving families, not investors, developers, or people owning multiple properties. The government has clearly defined who the scheme is meant for so that the benefit reaches the right people. Only permanent residents of Punjab can apply, and the applicant must represent the household officially.

From what I have observed, many applications fail simply because the wrong family member applies. The system only accepts applications from the NADRA-verified head of the household, ensuring accountability and proper repayment responsibility.

The scheme primarily targets:

- Families owning land but living in rented houses

- Low-income households excluded from bank loans

- Citizens with no constructed residential property

Applicant Identity Conditions Checked During Registration

Identity verification is the first and most critical step in the ACAG application process. The system cross-checks applicant information directly with NADRA records, leaving little room for manual interference. This ensures that loans are issued only to genuine Pakistani citizens.

Applicants must be adults and officially listed as the head of the family in NADRA data. In many rejected cases I have seen, the land belonged to the family, but the applicant was not registered as the household head, which caused automatic rejection.

Identity requirements include:

- Valid Pakistani CNIC

- NADRA family registration confirmation

- Applicant must be 18 years or older

Plot Ownership Rules You Must Satisfy Before Applying

Plot ownership is the backbone of the ACAG scheme. Without land registered in your own name, the application cannot proceed further. This loan is strictly for construction, not for buying land, which is why ownership verification is taken very seriously.

The government has also set size limits to prevent misuse. Small residential plots are allowed so that the scheme benefits ordinary families rather than large property holders.

Key plot ownership conditions:

- Applicant must be the sole legal owner

- Urban plot size must not exceed 5 Marla

- Rural plot size must not exceed 10 Marla

- Ownership must exist before submitting the application

Income and PMT Score Assessment Explained Simply

To make sure the loan reaches poor and deserving families, the government checks the monthly household income and the PMT (Poverty Means Test) score. The PMT score is already available in NSER and BISP records and reflects a family’s economic condition.

Only families earning PKR 60,000 or less per month and having a PMT score of 60 or below are considered eligible. This automatic filtering system ensures fairness and prevents financially stable households from benefiting unfairly.

Financial eligibility checks focus on:

- Total household income

- PMT score from NSER/BISP database

- Consistency between declared income and records

Social and Legal Background Screening

Beyond income and land ownership, the ACAG system also performs social and legal background checks. These checks protect public funds and ensure the loan goes to responsible citizens.

Applicants who already own a constructed house anywhere in Pakistan, have defaulted on bank loans, or have a criminal or anti-state record are not eligible. These checks are automated and difficult to manipulate.

Disqualifying conditions include:

- Ownership of any constructed residential house

- History of bank loan default

- Criminal or anti-state involvement

Documents You Should Prepare Before Starting Online Registration

From practical experience, applicants who prepare their documents before starting the application process face fewer delays and rejections. The ACAG portal is strict about document clarity and accuracy, and unclear uploads often result in verification issues.

All documents should be scanned clearly, with visible text and correct orientation. Using outdated or unreadable documents is one of the most common reasons for rejection.

Preparation guidelines:

- Use original documents for scanning

- Ensure documents are readable and updated

- Avoid submitting cropped or blurred images

Personal Identification Files Required by the Portal

The portal requires basic identity documents to confirm who you are and how you are linked to your family. These records help prevent fake or duplicate applications and ensure correct family mapping.

Many applicants ignore the importance of submitting the CNIC of a father or husband, which is essential for family verification.

Required identity documents:

- Applicant CNIC (front and back)

- CNIC of father or husband

- Recent passport-size photograph

Acceptable Proofs That Confirm Plot Ownership

To verify land ownership, the government accepts several official documents. Only one valid document is required, but it must be legally recognized and updated.

Submitting outdated or unofficial land papers often leads to rejection, even if the land genuinely belongs to the applicant.

Accepted ownership proofs include:

- Fard (ownership certificate)

- Registry or sale deed

- Allotment letter

- Mutation (Intiqal)

Income Verification Evidence for Different Applicants

Income proof requirements vary depending on how the applicant earns. Salaried individuals submit salary slips, while daily wage earners or self-employed persons submit an income undertaking.

Although NSER or PMT slips are optional, they help align the application with government records and strengthen credibility.

Income-related documents:

- Salary slip for employed applicants

- Income undertaking for laborers or self-employed

- NSER/PMT slip (optional)

Digital Declarations You Must Agree to During Submission

During online submission, applicants must accept legal declarations confirming that the information provided is true. These declarations are binding and can be reviewed later.

If any declaration is found false after approval, the loan can be cancelled and legal action may follow.

Applicants must declare:

- They do not own any other house

- The loan will be used only for construction

How the Loan Is Approved and Released After Registration

After submission, the application goes through multiple verification stages. Once approved, the loan is not released all at once. Instead, funds are released in construction-linked installments to ensure proper use.

Applicants can track their application and disbursement status online, which reduces confusion and unnecessary visits to government offices.

Approval process highlights:

- Digital record verification

- Field checks if required

- Tranche-based loan release

Key Loan Features Every Applicant Should Understand

Understanding loan terms helps families plan construction and repayments realistically. The ACAG loan offers fixed terms for all approved applicants.

| Feature | Details |

|---|---|

| Maximum Loan Amount | Up to PKR 1.5 Million |

| Interest Rate | Zero Interest |

| Loan Duration | 7 Years |

| Monthly Installment | Around PKR 14,000 |

| Disbursement Method | Construction-based installments |

Practical Tips to Increase Approval Chances

Successful applicants usually ensure that all records match across NADRA, land, and income databases. Small inconsistencies can delay approval or cause rejection.

Following basic precautions can significantly improve approval chances:

- Ensure NADRA and land records match

- Upload clear and correct documents

- Provide honest income information

Final Thoughts

The Apni Chhat Apna Ghar Construction Loan is one of the most practical housing initiatives introduced by the Punjab Government. It does not promise luxury, but it offers stability, dignity, and security to families who have waited years to build a home.

If you meet the eligibility criteria and prepare your documents carefully, this scheme can transform an empty plot into a permanent home. For many families, 2026 could finally be the year when the dream of owning a house becomes a reality.